It’s Not Always Positive

Ask a biotech CEO what their company is worth, and they’ll walk you through the science. The mechanism of action. The clinical data. The addressable market. Ask a venture investor the same question, and they’ll tell you something different: they’ll describe the team.

Not the org chart, but the capability architecture. Who’s making decisions, when they arrived, what they’ve done before, and whether the organizational design matches the stage. Investors don’t just model your pipeline. They model your team’s capacity to execute against the next value inflection, and they price it accordingly.

Here’s the uncomfortable truth: team composition in biotech isn’t an HR question. It’s a capital allocation decision. And like most capital allocation decisions, it’s subject to the same forces we’ve explored in previous work: the same valuation traps, the same narrative gaps, the same disconnect between how value is measured and how it actually accrues.

Get your team architecture right, and you compound value at every stage. Get it wrong, and you dilute. Not just through the cap table, but through burned runway, misread signals, and the quiet erosion of investor confidence that shows up at your next financing as a compressed valuation.

The Biology of Team Development

There’s a useful analogy from the science many of our clients know best.

In developmental biology, stem cells don’t simply multiply; they differentiate. At each stage of development, cells specialize into the tissue types the organism needs at that moment. Premature differentiation doesn’t accelerate growth. It produces dysfunction. A cell that tries to become cardiac tissue during gastrulation doesn’t build a stronger heart; it creates a developmental anomaly.

Biotech organizations follow the same logic. The team that’s right for discovery is wrong for pivotal-stage execution. The leadership profile that drives a company from IND to proof-of-concept is often mismatched to the demands of commercial launch. This isn’t a failure of the people involved. It’s a failure to recognize that team composition is stage-dependent, and that the wrong profile at the wrong time isn’t just a suboptimal hire; it’s a value-destructive event.

Consider one of the most consequential timing decisions in biotech: when to bring on a Chief Medical Officer. Hire too late, and you enter IND-enabling work without the clinical perspective that shapes protocol design, endpoint selection, and regulatory strategy from the start. The cost isn’t just a delayed timeline; it’s a clinical program that was architected without the judgment it needed, which compounds into downstream risk that investors will eventually price. Hire too early, before the translational science is mature enough to warrant a dedicated clinical leader, and you’re carrying senior compensation against a program that isn’t ready for what that person does best. The CMO isn’t failing; the organization is misallocating a scarce resource. Both errors look different on the surface, but they produce the same outcome: value that leaks quietly, showing up not on the income statement but in the term sheet.

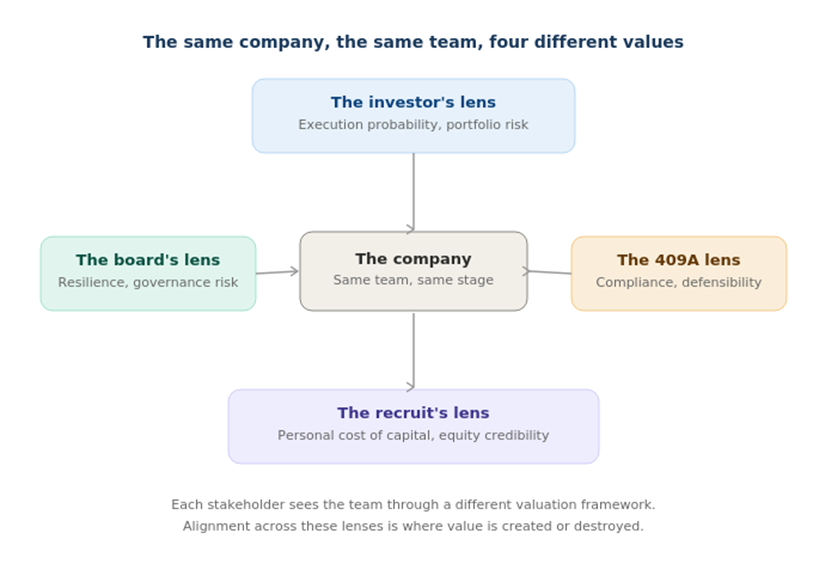

Value Is a Matter of Perspective, and So Is Team

One of the themes we’ve explored in earlier work is that the same biotech asset can carry multiple legitimate values simultaneously, depending on who’s looking and why. The 409A valuation serves a compliance purpose. The investor’s portfolio mark reflects a market thesis. The board’s strategic view incorporates optionality that neither number captures. These aren’t contradictions; they’re different lenses on the same underlying reality.

Team composition creates the same complexity of perspective, and understanding this is critical for leaders who want to manage value rather than just measure it.

The investor’s lens. VCs and crossover investors evaluate team composition as a forward-looking probability indicator. They’re asking: does this team have the pattern recognition to navigate the next eighteen months of value-creating milestones? A seasoned regulatory strategist joining at the IND-enabling stage isn’t just an operating expense; it’s a signal that increases the perceived probability of successful IND filing, which directly impacts the risk-adjusted valuation of the asset. Conversely, organizational gaps at critical junctures, such as no CMC leadership heading into process development or no finance leader who understands biotech capital structure heading into a Series B, register as execution risk and get priced accordingly.

The board’s lens. Directors see team through a governance and risk frame. Are we building organizational resilience, or are we creating key-person dependency? Is the leadership team evolving at the pace the company requires, or are we carrying a preclinical management structure into a clinical-stage enterprise? The board’s job is to ensure the team matches the company’s risk profile, and to manage the most sensitive transitions, particularly the founder-CEO evolution, which is itself a valuation event.

The recruit’s lens. This is where most companies underinvest in their thinking, and where the connection to valuation becomes most concrete. Senior hires in biotech evaluate equity compensation through the same probabilistic frameworks that investors use, whether they articulate it that way or not. A Chief Medical Officer weighing two offers is implicitly calculating: What’s the risk-adjusted value of this equity? How much dilution sits between here and an exit? Does this team have the capability to reach the milestones that would make my equity worth something?

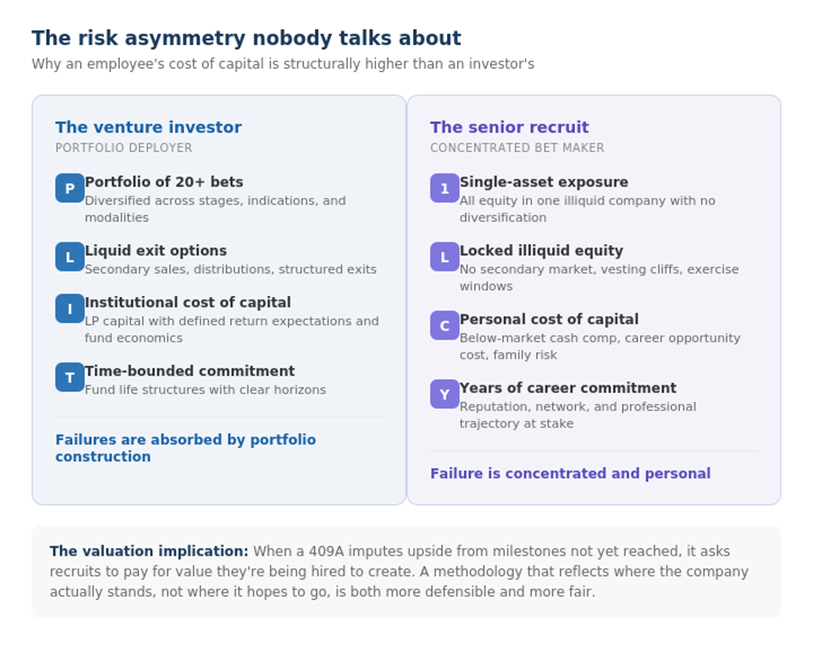

But there’s a crucial asymmetry that most valuation conversations ignore. An employee’s relationship to risk is fundamentally different from an investor’s. A venture fund deploys capital across a portfolio, expecting most bets to underperform and a few to generate outsized returns. The portfolio construction absorbs individual failures. An employee, by contrast, is making a concentrated bet. They’re committing years of their career, often accepting below-market cash compensation, and holding equity in a single illiquid asset with no ability to diversify that exposure. Their personal cost of capital, if we’re honest about it, is much higher than the institutional investor sitting across the cap table.

This asymmetry makes the question of how equity is valued acutely personal. And it surfaces a fairness problem that too few boards think about carefully: when a 409A or any valuation framework automatically imputes upside from value that has not yet been created, it penalizes the very people the company is trying to attract. A preclinical company whose common stock valuation bakes in assumptions about clinical milestones that haven’t been reached, regulatory outcomes that haven’t been achieved, and commercial potential that hasn’t been validated is, in effect, asking recruits to pay for future vale they’re being hired to help create. The employee is buying in at a price that reflects their own unrealized contributions. That’s not just a technical valuation question; it’s a question of organizational integrity.

This is precisely where rigorous, defensible 409A valuations become a strategic asset rather than a compliance obligation. When a 409A is anchored in methodology that reflects how biotech value actually moves, in milestone-driven steps rather than linear ramps, it gives companies a powerful recruiting tool. A thoughtfully constructed valuation that captures the company’s true position relative to its next inflection point allows management to present equity compensation with credibility. The candidate can see that the valuation reflects the science, the risk, and the opportunity, not just an audit-driven exercise in conservatism, and not a framework that charges them for the value they haven’t yet built.

Companies that treat their 409A as a box to check miss this entirely. Companies that treat it as a strategic instrument, one that accurately represents value and supports the narrative they’re building with recruits, investors, and partners, create a compounding advantage in the talent market.

Stage-by-Stage: What to Build, What to Contract, What to Automate

The practical question for biotech leaders isn’t just who to hire. It’s how to assemble capability, and that question now has more answers than it used to. The traditional binary of “hire full-time or outsource to a CRO” has expanded. Today’s biotech can build through full-time employees, fractional and contract specialists, outsourced partners, and increasingly, intelligent systems that augment human capacity. The right mix at each stage determines both capital efficiency and execution quality.

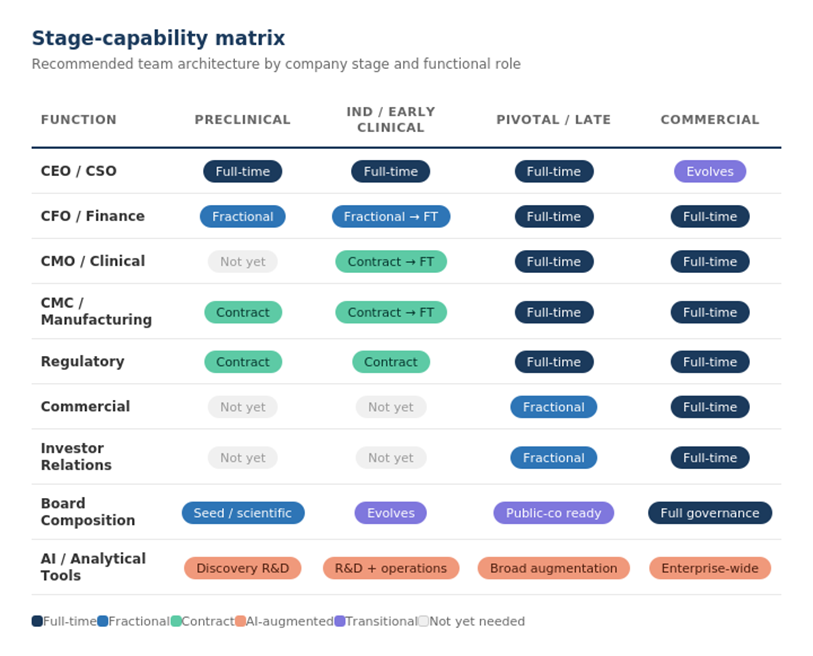

Preclinical and Discovery

At the earliest stages, capital efficiency is oxygen. Every dollar of burn rate that doesn’t advance the science toward proof-of-concept is a dollar of dilution at the next financing. In the current market environment, minimizing time and cost to proof-of-concept has become a defining priority for the most innovative companies we work with.

The core team should be small and senior: scientific founder or CSO, a program lead with translational depth, and a finance leader, almost always fractional at this stage. A fractional CFO who has navigated dozens of biotech cap tables, fundraising cycles, and 409A processes brings more strategic value two days a week than a junior full-time hire brings in five. Regulatory input should come from an experienced consultant on defined deliverables, not a full-time head of regulatory affairs.

The mistake that destroys value at this stage is premature organizational scaling. Building out a C-suite before the science justifies it doesn’t demonstrate vision; it demonstrates a misunderstanding of what stage you’re in. Investors see it. They adjust.

The exception: platform companies with multi-program potential may need deeper technical leadership earlier, a CTO or Head of Chemistry whose role is to build the engine, not just advance one program.

IND-Enabling Through Early Clinical

This is where the organization begins to differentiate, where stem cells start becoming tissue. The company needs CMC capability (transitioning from contract to dedicated as molecule complexity demands it), clinical operations oversight (even if CRO-managed, someone must own clinical judgment internally), and increasingly, a finance leader who can navigate the capital structure decisions that become continuous rather than episodic as the company approaches its next inflection.

The full-time CFO trigger is usually tied not to company size but to capital markets complexity. When you’re actively planning a financing round, managing investor relationships, and making decisions about capital structure that will compound for years, you need a dedicated finance leader who can think in biotech-specific terms, not a generalist, and not a consultant you talk to once a month.

Fractional and contract specialists remain valuable here for functions that are important but episodic: IP strategy, HR and people operations, investor relations groundwork. The key discipline is distinguishing between roles that require institutional continuity (these should be full-time or deeply embedded fractional) and roles that require periodic expertise (these should be contract).

Pivotal and Late-Stage Clinical

The organizational demands shift markedly. Medical affairs often starts as a contract engagement and converts to full-time as the company approaches the data that will define its commercial trajectory. Commercial strategy, not execution but strategy, should begin in earnest, often through a fractional Chief Commercial Officer or market access advisor who can pressure-test assumptions without the burn rate of a full commercial build.

Investor relations capability becomes essential, particularly for companies on the IPO track. This is a chronically underutilized fractional role. Pre-IPO companies rarely need a full-time IR professional, but they absolutely need someone who can build the investor book, refine the narrative, and manage the communication cadence. The cost of getting this wrong isn’t measured in salary; it’s measured in IPO pricing.

Board composition should evolve in parallel. Directors with public-company experience, commercial-stage pattern recognition, and genuine operating relevance replace the seed-stage board that served its purpose at formation. Board composition is one of the most underweighted valuation levers available. The right director at the right stage can be worth more than a full-time hire in credibility, network access, and strategic judgment, all without adding to the burn rate.

Commercial Transition

This is where the virtual model reaches its structural limits. You cannot launch a product with a collection of contracts. Commercial execution demands integrated, full-time leadership across sales, medical affairs, market access, supply chain, and commercial operations. The transition from virtual to operational organization is one of the most dangerous periods in a biotech’s life; culture fractures, burn rates spike, and the coordination complexity that was manageable at ten people becomes unmanageable at seventy.

The companies that navigate this transition well make it a deliberate strategic process, not an emergency response to an approval date. They begin embedding commercial DNA eighteen to twenty-four months before anticipated launch. They think about cultural integration as seriously as they think about launch sequencing. And they recognize that the scientific founder who built the platform may not be the right CEO for a commercial-stage enterprise, and that how that transition is managed sends a signal to every stakeholder watching.

Virtual, Scaled, or Hybrid: A Structural Decision

The choice of team architecture isn’t just operational. It’s strategic, and it should be made deliberately, not by default.

Virtual companies optimize for capital efficiency, flexibility, and speed to proof-of-concept. They minimize fixed costs, extend runway, and reduce dilution per unit of time. But they pay for it in institutional knowledge fragility, coordination overhead that doesn’t appear on the income statement but shows up in timeline slippage, and investor concern about whether there’s a durable organization behind the science.

Scaled enterprises optimize for proprietary capability, multi-program execution, and organizational resilience. They build institutional learning and cultural cohesion. But they carry higher burn rates, develop organizational inertia that makes pivoting painful, and face the “overhead trap,” where once the machine is built it needs to be fed, which can drive suboptimal program decisions.

The strategic question for boards is straightforward: which architecture matches your value-creation thesis? A single-asset company pursuing one pivotal readout should almost never build a scaled enterprise. A platform company with three programs and a discovery engine probably can’t stay fully virtual. The mistake isn’t choosing wrong; it’s not choosing at all, and drifting into an architecture that serves neither the science nor the capital structure.

The Emerging Variable: AI and the Hybrid Organization

There’s a third model taking shape, and it changes the calculus in ways that matter for both operators and investors.

Many of the biotech companies we work with are already integrating AI-driven capabilities on the discovery and R&D side: computational chemistry, target identification, preclinical modeling. That adoption curve is accelerating, and it’s extending into operational domains that have traditionally required dedicated headcount, including regulatory intelligence, competitive landscape monitoring, financial scenario analysis, data management, and compliance workflows.

The implication isn’t that AI replaces teams. It’s that AI changes the optimal composition of teams at every stage. A small, senior core augmented by intelligent systems can achieve execution quality that previously required significantly more headcount, and the capital efficiency gains are meaningful. Not in the abstract, but in concrete terms: extended runway, fewer dilutive financings, and stronger negotiating position at each capital raise.

But the premium doesn’t go to companies that use AI as a substitute for expertise. It goes to companies that use it as a multiplier of senior judgment. A regulatory strategist augmented by AI-driven intelligence scanning is dramatically more productive. A finance team supported by automated scenario modeling can evaluate strategic options in hours rather than weeks. These are capability enhancements, not headcount replacements, and investors are learning to tell the difference.

Ironically, this shift makes human recruiting decisions more important, not less. When your core team is smaller and more leveraged, each hire carries more weight. A mis-hire at the preclinical stage in a twelve-person company is costly. A mis-hire in a six-person hybrid organization, where that individual is responsible for an entire functional domain augmented by AI but ultimately accountable for judgment, is existential. The quality of each human decision-maker goes up, not down, as intelligent systems absorb more of the execution layer.

This is where the connection back to valuation becomes acute. If each senior hire matters more, then the tools that support recruiting, including equity compensation frameworks grounded in rigorous, stage-appropriate valuations, matter more too. A company that can demonstrate to a prospective CMO or Head of Regulatory that its equity is valued with real analytical sophistication, not just compliance-grade conservatism, has a structural advantage in the talent market. That advantage compounds as the hybrid model makes every hire more consequential.

The Compounding Logic

The thread that runs through all of this, from team architecture to stage-appropriate composition to virtual vs. scaled vs. hybrid to the fact that value is always a matter of perspective, is that team decisions compound. They don’t just affect the current quarter’s burn rate. They affect the signal you send to investors about organizational self-awareness. They affect your ability to recruit the senior talent that drives the next milestone. They affect the cultural DNA that either enables or resists the organizational evolution your company will inevitably require.

Biotech value doesn’t move linearly. It moves in steps, and the team you build determines whether you’re positioned to capture each step or whether you arrive at the staircase with the wrong shoes on.

The companies that treat team composition as a capital allocation decision, with the same rigor they apply to pipeline prioritization, clinical trial design, and capital structure, are the ones that compound value through every phase transition. The ones that treat it as an afterthought, or a founder’s prerogative, or an HR function disconnected from strategy, are the ones whose term sheets eventually tell the story of value that was created in the lab but lost in the org chart.

Your team isn’t just building the company. Your team is the company, as seen through every lens that matters.

About RNA Advisors

RNA Advisors helps biotechnology and pharmaceutical companies translate scientific and clinical value into investor-ready narratives. Our valuation frameworks are built specifically for milestone-driven biotech—modeling phase transitions/value inflection points explicitly, aligning methodology to the actual market participants at each stage of development, and preserving the optionality that standard approaches tend to flatten. Through rigorous financial modeling, market research, and analytical frameworks built for the unique dynamics of life science assets, we bridge the gap between breakthrough science and effective capital formation.