[Extended JPMSA article summary]

The financial tools most life-science companies use to value assets, structure transactions and allocate capital were built for stable systems. Drug development, market access and biotech exits are not stable systems.

The result is not just forecast error. It is decision error: mistimed financings, mis-scoped launches, suboptimal evidence plans and avoidable misalignment in transaction economics.

In our recent paper for the Journal of the Pharmaceutical Management Science Association, we propose an alternative framework. It does not replace rNPV, scenario analysis or cap-table modeling. It extends them. The goal is not analytical sophistication for its own sake; it is practical improvement in how life-science organizations make decisions under genuine uncertainty.

The Problem with Point Estimates

Traditional rNPV models generate single “most likely” projections for peak sales, market share, pricing and development timelines. These point estimates create an illusion of precision that obscures the true range of possible outcomes.

Life-science returns follow a power law. A small number of programs generate outsized returns; the majority produce modest or negative value. Smoothing this reality into averages simultaneously understates downside risk and upside opportunity, leading to systematically biased capital allocation.

The problem compounds when static assumptions meet dynamic environments. Patient response varies across subpopulations. Physician adoption follows network-mediated diffusion, not smooth S-curves. Payers adjust coverage in response to accumulating evidence. Competitors react strategically to successes and failures in adjacent programs. Regulatory and HTA expectations shift with class experience.

These interactions create feedback loops and path dependence that spreadsheet models are structurally unable to represent.

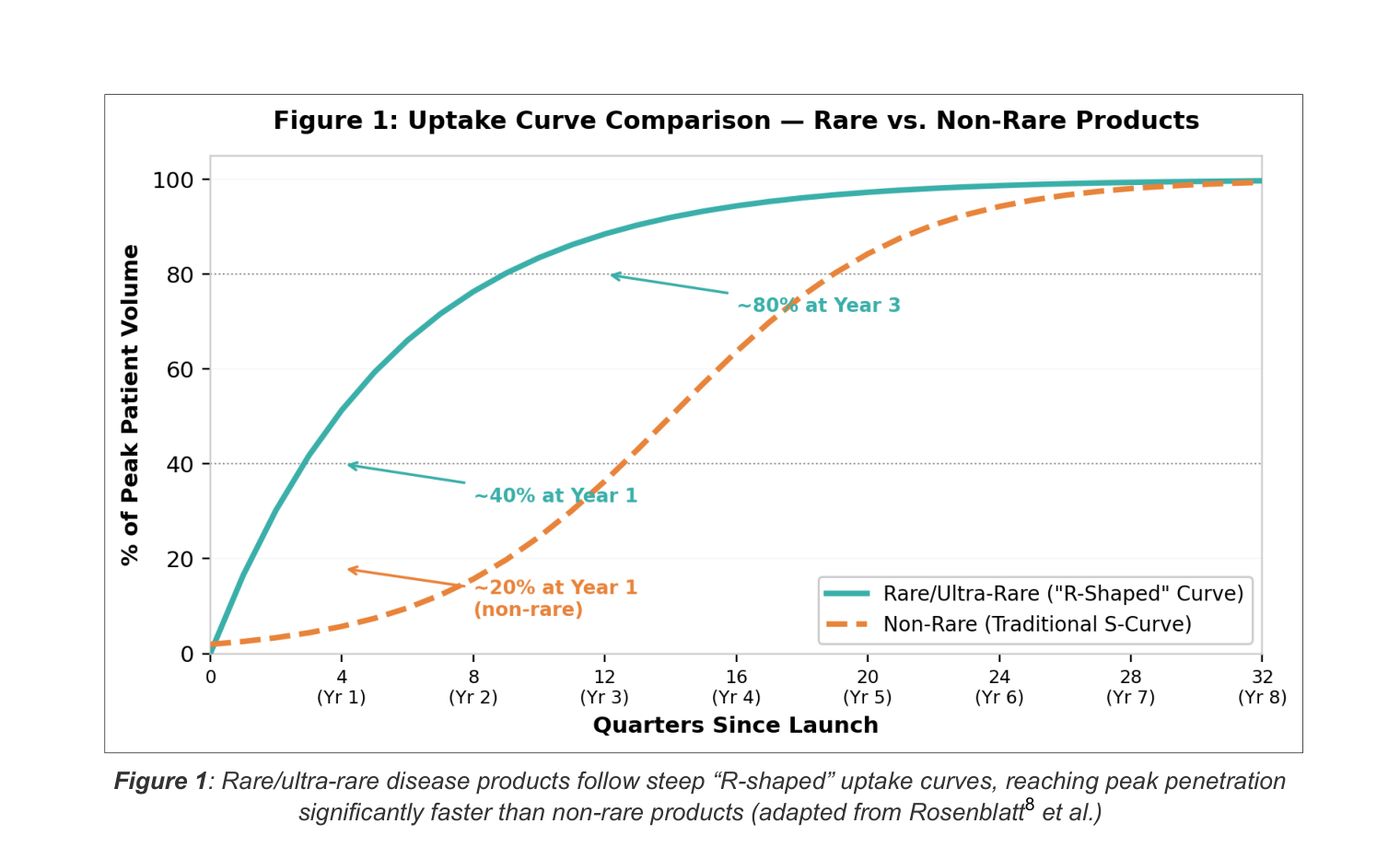

Empirical Evidence: The R-Shaped Curve

A practical signal that static assumptions are breaking down is the shape and speed of adoption. Recent empirical work, drawing on longitudinal claims data, has shown that rare and ultra-rare disease products follow distinctly steep “R-shaped” uptake curves, reaching roughly 40% of peak patient volume within the first year and peak penetration within five years. Non-rare products, by contrast, take eight years or more to reach the same plateau.

This is not a marginal modeling adjustment. A forecast that assumes an S-curve for an R-shaped product will systematically misprice the asset, mistime the financing and miscalibrate the launch investment.

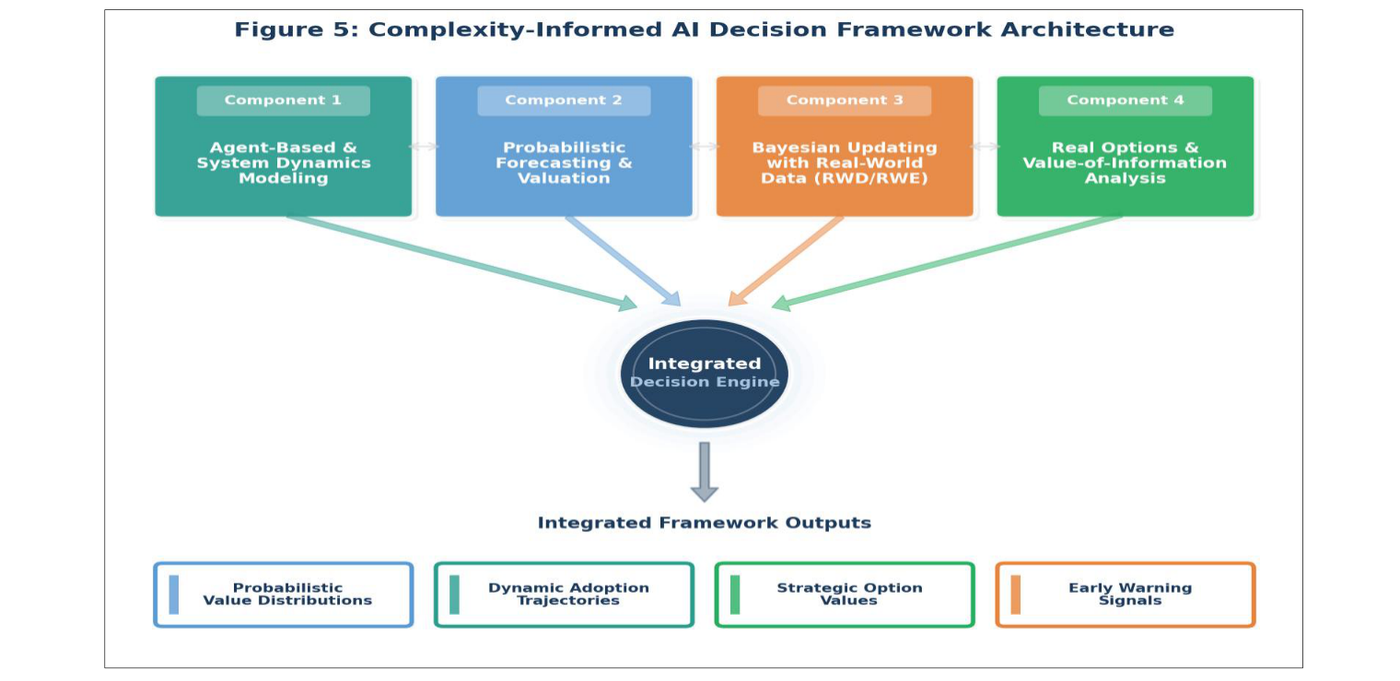

The Framework: Four Complementary Components

We propose four complementary analytical components. Organizations can adopt them incrementally; the greatest value, however, arises from their integration.

Component 1 — Agent-based and system dynamics modeling. Aggregate assumptions get replaced with explicit behavioral models of stakeholder groups. Physician prescribing decisions are simulated as functions of evidence exposure, peer influence, formulary access and patient outcomes. The output is adoption trajectories that reflect network-mediated, nonlinear patterns observed in actual pharmaceutical markets.

Component 2 — Probabilistic forecasting and valuation. Point estimates get replaced with probability distributions. Monte Carlo simulation generates thousands of valuation scenarios by sampling from distributions of clinical endpoints, pricing outcomes, market timing and competitive entry. The output is not a single NPV but a distribution of asset values.

Component 3 — Bayesian updating with real-world evidence. Model assumptions get refreshed systematically as new data arrive. Real-world data from electronic health records, claims databases, registries and post-marketing surveillance provide continuous signals about treatment response, adoption and safety, updating prior assumptions throughout the development lifecycle.

Component 4 — Real options and value-of-information analysis. Committed-pathway thinking gets replaced with explicit valuation of managerial flexibility. An early-stage program is a portfolio of options whose value depends on volatility, the cost of exercising the next stage and the time before decisions must be made. Value-of-information analysis directs evidence-generation resources toward the highest-value uncertainties.

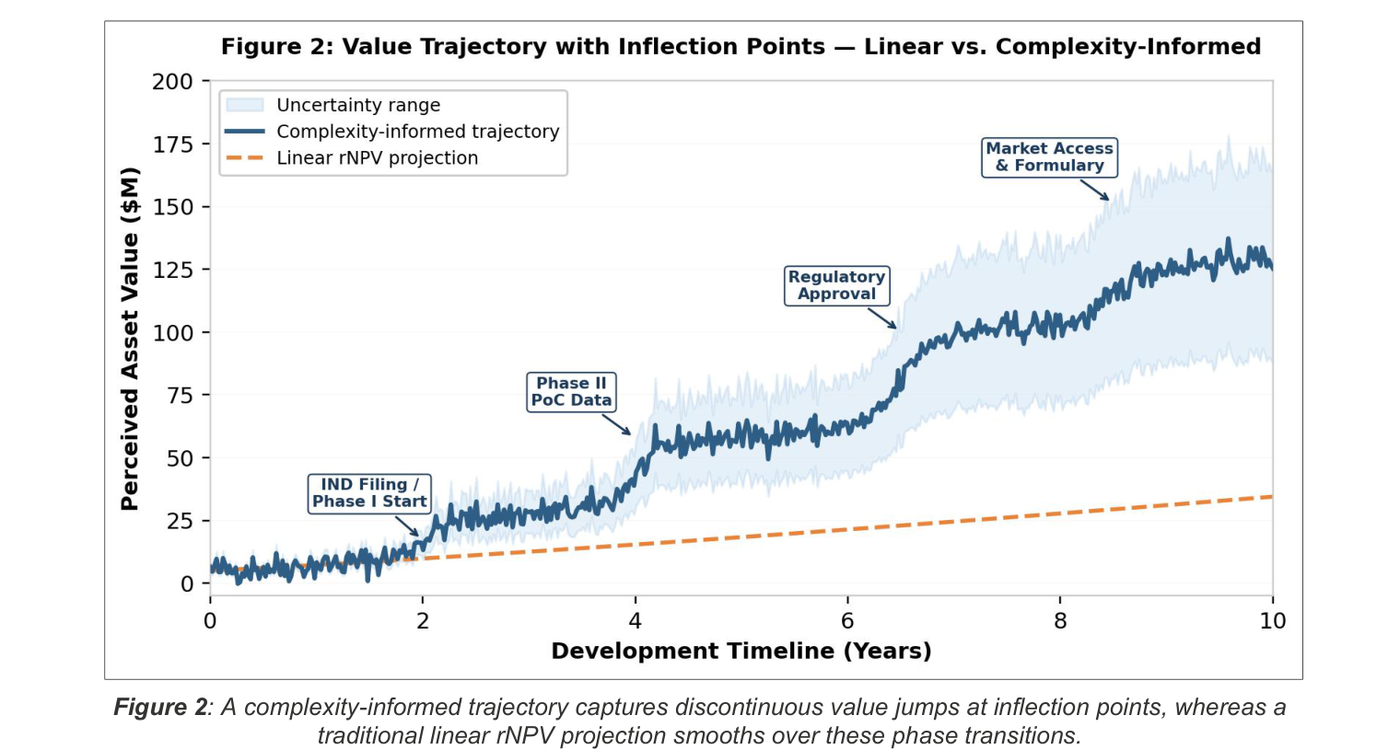

Inflection Points: The Cost of Linear Thinking

A linear rNPV projection draws a smooth, gradually rising line. A complexity-informed trajectory captures discontinuous value jumps at inflection points: IND filing, Phase II proof-of-concept, regulatory approval, market access. The same underlying asset can experience meaningful value increases without a proportional change in “expected” outcomes, because the market’s capacity to fund, price and realize those outcomes has changed.

Missing those inflection points, or modeling them as gradual ramps, is one of the most common and most expensive errors in life-science capital decisions.

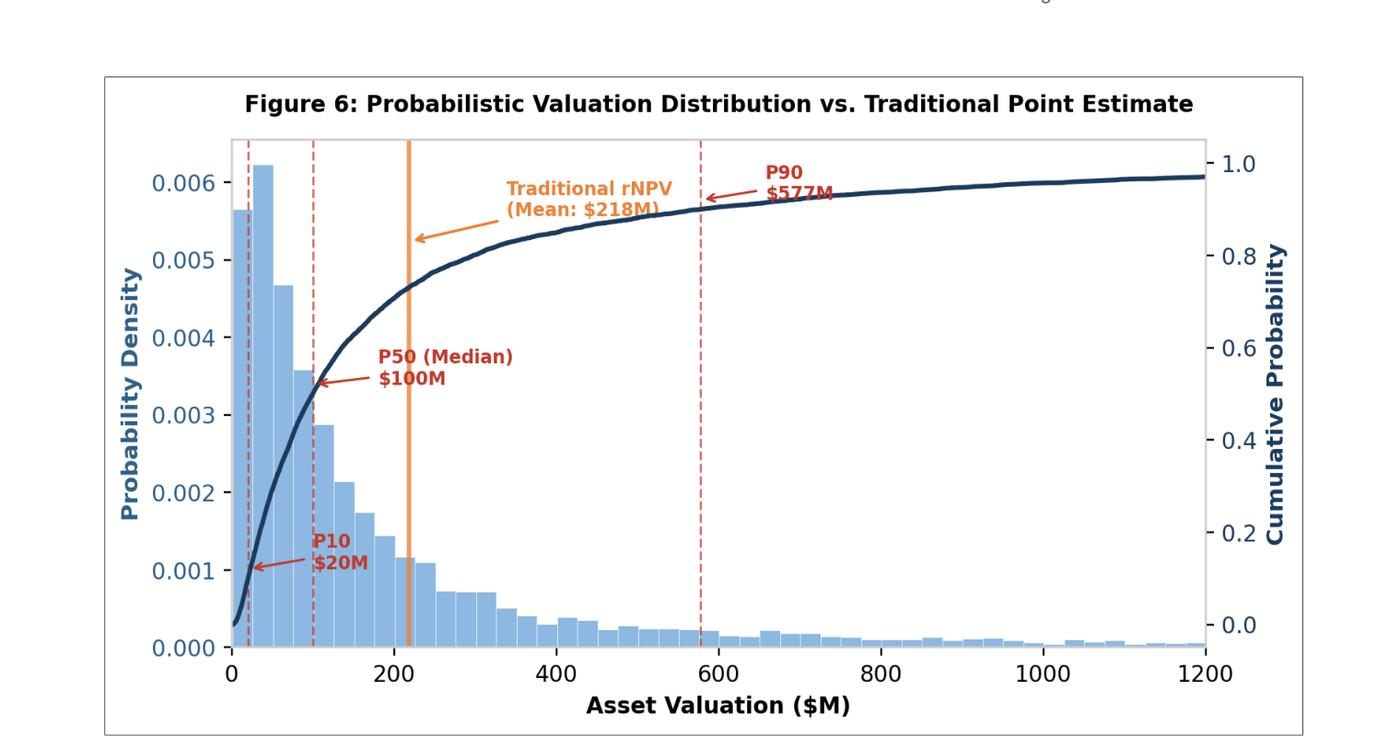

The Headline Finding: The Mean Versus the Median

The most consequential illustration of why distributions matter is what happens when one is generated. A Monte Carlo simulation of 10,000 scenarios for a hypothetical asset produces a traditional rNPV of roughly $218M, which corresponds to the arithmetic mean of the distribution. The median outcome is roughly $100M, less than half that figure. The gap is not error. It is the heavy right tail of a power-law distribution pulling the average upward.

A decision-maker anchored on $218M believes they are reasoning about a “likely” outcome. In fact, they are reasoning about a value that no realistic outcome path actually produces. The strategic conversation changes when the distribution is in front of you. The relevant questions become: What is the probability this asset exceeds our minimum return threshold? Which uncertainties, if resolved, would most shift the shape of the distribution? Which evidence-generation activities are worth their cost?

What This Changes in Practice

For executives, boards, investors and counsel making real decisions, the framework supports five practical shifts:

- Forecasts that reflect network diffusion and payer feedback, not only smooth penetration curves.

- Valuations expressed as distributions with tail behavior, not single numbers that hide bimodal reality.

- Adaptive updates that incorporate clinical readouts, payer decisions and early launch signals as formal Bayesian evidence updates.

- Explicit valuation of managerial flexibility — the option to expand, defer, partner or abandon — with prioritization of the highest-value uncertainty-reduction activities.

- Cap-table and term-sheet analysis that forecasts incentive alignment and preference-overhang dynamics under realistic exit distributions.

About the Authors

Samuel Renwick, CFA is Founding Principal of RNA Advisors. Sam advises pharmaceutical and biotechnology companies on complex financing architectures, partnering decisions and portfolio strategy, bringing a systems-oriented perspective to capital allocation under uncertainty. Prior to founding RNA, Sam led the life-science team at SVB Analytics. He is the recipient of the J. Fred Weston award from UCLA Anderson for excellence in finance.

Jerry A. Rosenblatt, PhD is Founding Principal of Rosenblatt Life Science Consultants. Jerry has spent more than thirty years applying scientific methods to pharmaceutical forecasting, opportunity assessment and business valuation. He is the former Head of the Global Forecasting & Opportunity Assessment consulting group of IMS Health (now IQVIA) and a recipient of the PMSA Lifetime Achievement Award.

About RNA Advisors

RNA Advisors helps biotechnology and pharmaceutical companies translate scientific and clinical value into investor-ready narratives. Our valuation frameworks are built specifically for milestone-driven biotech — modeling phase transitions and value inflection points explicitly, aligning methodology to the actual market participants at each stage of development, and preserving the optionality that standard approaches tend to flatten. Through rigorous financial modeling, market research, and analytical frameworks built for the unique dynamics of life science assets, we bridge the gap between breakthrough science and effective capital formation.