Unfortunately, this actually happened.

I. The Worldview Before the Story

Every transaction begins before the first term sheet is drafted. Before the first handshake, every participant has already decided what kind of story they’re living in. The deal doesn’t create the narrative. The deal is where pre-existing narratives collide, and the outcome depends entirely on whether those narratives are compatible.

This is a story about a biotech company where every participant told themselves a true story, and the collision destroyed them all.

II. The Company

The company had the ingredients. A validated target in a therapeutic area experiencing one of those periodic surges of investor enthusiasm, the kind of moment when conference presentations draw standing-room crowds and BD teams from every major pharma start returning emails the same day. Early data was encouraging. The science was credible. The existing team had brought the program to a stage where the next move was obvious to everyone: bring in a CEO who could capitalize on the window.

The board, dominated by the institutional investors who had funded the company through its first rounds and led by a partner whose background was primarily in technology, understood this in terms they knew well. The company needed an upgrade. A proven operator who could close a Series B in a hot market, build out the clinical organization, and position for the next inflection point. They had built the vehicle. Now they needed someone to drive it.

The employees, the scientists and early hires who had taken below-market salaries and staked career years on the thesis, understood it differently, though they couldn’t have articulated the distinction. For them, the CEO hire wasn’t an upgrade. It was validation. Someone important was betting their career on the same thing they’d bet theirs on. The arrival of a top-tier CEO would confirm that the sacrifice had been worth it, that the equity they’d accepted in lieu of cash compensation was on its way to meaning something.

These two stories were compatible. For now.

III. The CEO

The CEO they recruited was exactly what the company needed, and he knew it. He had built companies before. He had relationships with the investors who would write the Series B check. He had the credibility to recruit the clinical team that didn’t yet exist. He understood, with the pattern recognition that comes from having done this more than once, that the company’s current trajectory was a direct function of whoever occupied his chair.

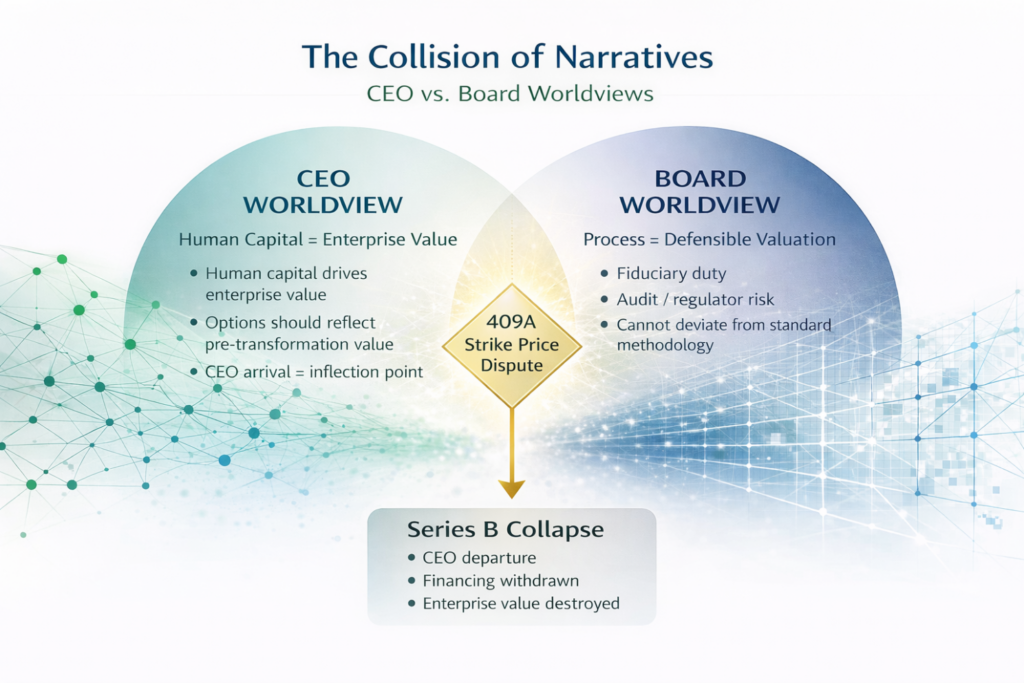

His story, the one he told himself, the one that was true, was simple: I am crucial to the next inflection point. Before me, this is a promising early-stage company with interesting science and a depleting bank account. After me, this is a funded clinical-stage enterprise with a clear path to value creation. The difference between those two things is me; my network, my judgment, my ability to execute.

This story was not arrogance. It was an accurate assessment of how value creation works in venture-backed biotech at this stage. The enterprise value set by the last preferred round was not a price for a self-sustaining business. It was a price for cash plus science plus people, and the largest single variable in the “people” component was about to change. The CEO understood, at a gut level even if he wouldn’t have used this language, that the company’s value before his arrival was substantially composed of potential that only someone like him could convert into reality.

He expected his option grant to reflect this. The strike price, in his worldview, should capture the company before the transformation he was about to catalyze, not after it. He was buying in at the ground floor of what his own effort would build. Every day that passed after his arrival, the value his options were supposed to capture was the value he was creating. Setting the strike price at a level that already reflected his presence was, to him, asking him to pay for his own contribution twice: once in the career risk and compensation sacrifice of joining, and again in the option price.

IV. The Board

The board’s story was equally true, and structurally irreconcilable.

The investors around the table had not built their careers by deviating from established practice. They operated within an ecosystem where the way things are done is not merely convention but survival strategy. A fund that structures deals unconventionally, that takes positions other firms wouldn’t take, that sets prices other auditors wouldn’t approve, creates questions. Questions from limited partners. Questions from co-investors. Questions that, regardless of whether the underlying decision was correct, threaten the ability to raise the next fund.

When outside counsel and the auditors flagged the strike price, the board heard something the CEO did not: if we get this wrong, the consequences cascade. A 409A valuation that can’t withstand scrutiny doesn’t just create a tax problem for the CEO. It creates an audit issue for the company, and audit issues can create problems in temperamental and sometimes open, sometimes closed public capital markets.

Their story was about process, discipline, and defensibility, especially through the lens of the lead investor’s technology sector experience. The methodology produces a number. The number is the number. You can argue with it at the margins, but you cannot simply assert that the number should be different because you believe your arrival changes everything. The board had seen executives overvalue their own contribution before. They had a fiduciary duty to the existing shareholders, including those early employees whose equity was also at stake. They could not set a strike price based on one person’s narrative about their own importance, however compelling that narrative might be.

V. The Collision

There is a moment in every unresolvable conflict when two authentic stories, each believed completely by its teller, each internally consistent, each supported by the teller’s lived experience, meet and discover they are mutually exclusive.

The CEO saw the board’s position as an insult to the economic reality of his contribution. He had left a comfortable position. He had staked his reputation on this company. And now the people who had recruited him were telling him, through the language of strike prices and valuation methodologies, that his arrival hadn’t changed anything, that the company was worth the same the day after he joined as the day before.

The board saw the CEO’s position as a governance red flag. An executive who, before even closing his first financing, was already fighting with the auditors over his own compensation terms was an executive whose priorities might not align with the company’s. They had seen this movie before, and it didn’t end well.

Neither side was wrong. That was the problem.

The CEO’s story, that his human capital was the dominant value driver and that pricing his options as if that value already existed in the enterprise was economically incoherent, was analytically correct. At this stage of development, the enterprise was its people. The methodology was treating a negotiated preferred price as evidence of going-concern enterprise value when, in reality, a substantial fraction of that value was personal goodwill that would leave with the individuals if they departed. Which is exactly what was about to happen.

The board’s story, that you cannot set a strike price based on a single executive’s self-assessment of their own value-add, that the methodology exists precisely to prevent this kind of subjective overreach, and that the reputational and regulatory consequences of getting it wrong would harm every stakeholder, was procedurally correct. They were applying the tools they had, in the way those tools were designed to be applied. The fact that the tools were designed for a different context, technology companies where value accrues to code and products rather than to specific scientists and executives, was not something the tools themselves could tell them.

VI. The Destruction

What happened next was predictable to everyone and preventable by no one, because each participant’s internal logic made their next move inevitable.

The CEO departed. Not quietly. Litigation was threatened. And the timing could not have been worse. The Series B was nearly complete. The CEO’s credibility, his relationships with the incoming investors, his personal commitment to the people writing the check; these were the load-bearing elements of a financing that was weeks, not months, from closing. His departure didn’t just damage the round. It destroyed it. The investors who had been prepared to commit tens of millions walked away, not because the science had changed, but because the human architecture that gave them confidence had collapsed overnight.

The financing window, the one created by the hot therapeutic area, the conference buzz, the BD interest, did not wait. Windows in biotech are environmental. They are created by the convergence of scientific momentum, investor appetite, and competitive dynamics. They open based on forces no single company controls, and they close the same way. This one closed.

The employees, the scientists who had accepted below-market compensation, who had told themselves the story that their sacrifice would be rewarded, absorbed the full downside. Their equity, already illiquid and structurally junior to the preference stack, became functionally worthless as the company teetered toward insolvency. They had no voice in the strike price dispute. They had no seat at the table where the stories collided. They were the audience that both storytellers forgot was in the room.

VII. What the Stories Couldn’t See

The deepest cruelty of this outcome is that the CEO’s departure proved his thesis. The company’s near-collapse after his exit was the most powerful possible evidence that enterprise value at this stage is dominated by human capital, that the “going concern” the methodology was pricing was, in fact, a collection of people whose departure could unravel everything.

But the proof came too late, and at a cost no one could afford.

The most dangerous stories are the ones where the teller is right. When a story is false, when the narrative doesn’t match reality, events eventually correct. The deception collapses under its own weight. But when the story is true, when the teller genuinely believes it because it genuinely reflects their experience and their position in the world, no amount of contradictory evidence will dislodge it. The teller holds on tighter, because to them the evidence confirms what they already knew.

The CEO believed his story more deeply after the board rejected it, they don’t understand what I bring. The board believed their story more deeply after the CEO pushed back, this is exactly why you need process discipline. Each participant’s response to the conflict reinforced the very worldview that made the conflict irresolvable.

And the people whose stories no one asked about, the early employees, the patients who would have benefited from the therapy, the scientific mission itself, paid the price for a collision between two true stories that no one had the structural position to mediate.

VIII. The Aftermath

The company didn’t die. It came close, and in some ways that has been worse.

In the years since, the existing investors have drip-fed capital into the company. Enough to keep the lights on. Enough to maintain the intellectual property. Not enough to advance the program with conviction. The therapeutic area that was once the darling of investor conferences has, as these things do, cycled out of favor. The standing-room crowds have moved on to the next hot target, the next wave of enthusiasm. The BD teams that once returned emails the same day now take weeks, if they respond at all.

And here is the bitter irony: the technology is still good. The science hasn’t changed. The target remains validated. The data that made the company compelling years ago is, if anything, more compelling now, as subsequent academic work has reinforced the thesis. What the company lacks is not scientific merit. What it lacks is the capital to be patient.

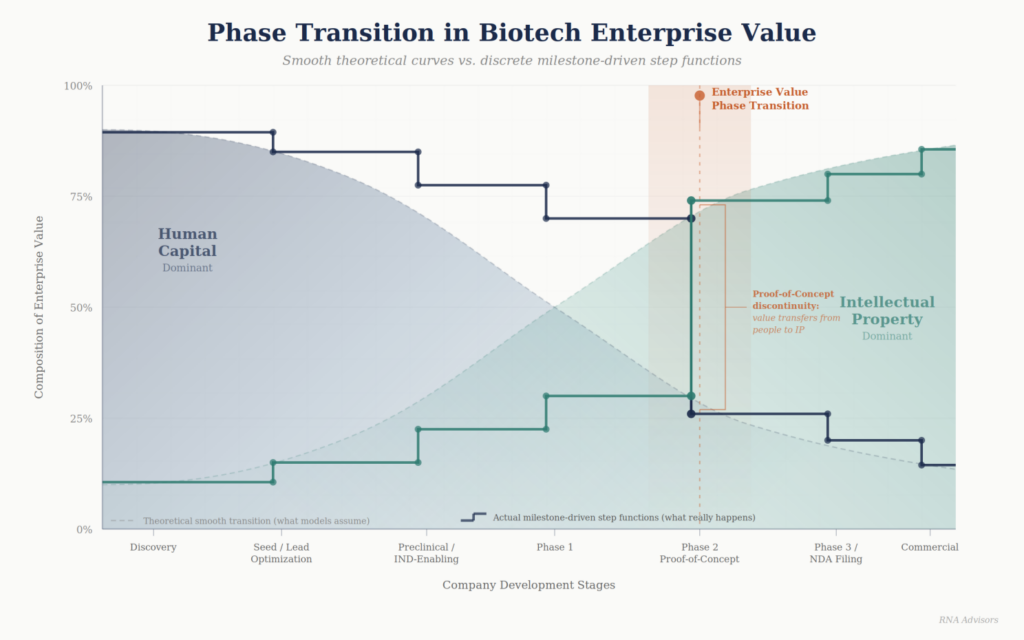

This is the lesson that gets lost in the wreckage. In biotech, the real phase transition, the moment when enterprise value shifts permanently from human capital to durable intellectual property, happens when proof-of-concept data arrives. Everything before that moment is prologue. And prologue requires patience, which requires capital, which requires a financing architecture that can absorb the inevitable cycles of investor enthusiasm and indifference without breaking.

A fully funded Series B would have given this company the runway to weather the shift in sentiment. It would have allowed the science to proceed on its own timeline rather than the market’s. It would have created the conditions for the program to reach the clinical milestone that would have rendered the strike price dispute, the CEO’s departure, and the therapeutic area’s fall from fashion all irrelevant. Proof-of-concept data has a way of rewriting every story that came before it.

Instead, the company exists in a state of suspended animation, kept alive by investors who have too much sunk cost to walk away but too little conviction to commit at scale. The employees who stayed, the ones whose loyalty outlasted the crisis, continue to work on a program they believe in, with resources that signal the opposite. The science waits. The window, when it reopens, may find a company too depleted to walk through it.

IX. The Story That Was Missing

In every venture-backed biotech company, there is a participant who, in principle, could have bridged these worldviews. Someone whose own experience spans both sides; who understands the CEO’s conviction that human capital is the enterprise at this stage because they’ve lived it, and who understands the board’s need for defensible process because they’ve sat in that room too. Someone who isn’t locked into the institutional logic that makes structural deviation feel existentially threatening.

At most early-stage biotech companies, that participant doesn’t exist. The capital intensity, the domain expertise requirements, the binary milestone structure, all of it conspires to eliminate the intermediary whose presence might have made the difference. Not someone who could have solved the valuation question, but someone who could have translated between the two authentic stories before they became mutually exclusive.

The absence of that translator is not an accident. It’s structural. And until the structures change, until the frameworks acknowledge that the same asset genuinely looks different depending on which story you’re living in, this collision will repeat. Different companies, different therapeutic areas, different names around the table. The same irreconcilable stories. The same destruction.

X. The Question Nobody Asked

The valuation methodology was designed for a world where enterprise value exists independently of specific individuals, where the “business” is a durable thing that persists regardless of who occupies which chair. That worldview is true for some companies at some stages. It is not true for a pre-revenue biotech whose principal asset is the scientific thesis and operational capability of a handful of irreplaceable people.

The CEO’s compensation expectations were designed for a world where the individual’s contribution is recognizable, measurable, and compensable at the moment of joining, where the strike price is a market’s acknowledgment of the before-and-after. That worldview is true in the CEO’s lived experience. It is not true in the auditor’s compliance framework.

Both stories were authentic. Both were told by people who believed them. And because no one in the room had the structural position to say both of these stories are true, and the job is to find the price that honors both, the stories collided, and the company that both stories were trying to serve was destroyed in the collision.

Every deal tells a story. The question is whether the participants recognize that they’re telling different stories, before the ending writes itself.

XI. The Translator That Was Never in the Room

This story did not have to end this way. The collision was not caused by bad actors, greed, or incompetence. It was caused by the absence of a translator.

Not a person, though a person might have helped. What was missing was a mechanism, a way of looking at the company that could hold both stories simultaneously and prove, with the rigor the board required and the economic honesty the CEO demanded, that both were valid. A framework that could say to the auditors: this executive’s human capital is the dominant component of enterprise value right now, and here is how we account for that. And say to the CEO: your contribution is real, it is measurable, and here is the price that reflects the company before your efforts compound, set on terms that will survive regulatory scrutiny and protect every shareholder at the table, including the scientists down the hall whose equity depends on this conversation going right.

The standard valuation methodology could not do this. It was not designed to. It was built for enterprises whose value resides in durable assets, code, products, customer relationships, things that persist regardless of who shows up on Monday. It works beautifully in that context. But a pre-revenue biotech is not that context. Its value lives in specific people doing specific work, and it will only become a durable enterprise after those people succeed. The methodology cannot see the difference between a company that has already made the transition and one that hasn’t started it yet. So it prices both the same way, and the price is wrong in both directions.

What would the translator have seen? It would have seen that the company existed in a specific developmental stage where the composition of its value, who created it, where it resided, how durable it was, determined how common stock should be priced. At this stage, most of the enterprise’s worth was inseparable from the people building it. The CEO was right about that. The framework would have adjusted for this personal goodwill before running any allocation model, producing an enterprise value that reflected what would survive a key departure rather than what existed with everyone in their seats.

It would have recognized that common stock at this stage functions primarily as a recruiting instrument, not an investment security. The relevant buyer is an employee evaluating a total compensation package, not an investor running an option pricing model. The strike price should reflect that employee’s revealed willingness to pay, the career risk and cash sacrifice they accept, not a mathematical allocation from a preferred round negotiated by investors with entirely different objectives and risk profiles.

And it would have produced a number. Lower than the standard option pricing backsolve, because the standard model overstates common’s value at this stage by treating the preference stack as a permanent feature of a going concern rather than a financing artifact in a human-capital-dominated enterprise. Higher than the CEO’s subjective sense of what his options should cost, because the framework is calibrated to empirical data, not personal conviction. Defensible to the auditors, because it is grounded in the same theoretical foundations they already accept. And functional as a recruiting tool, because the resulting strike price actually reflects what the equity is worth to the person being asked to bet their career on it.

Not a compromise. A better answer.

The technical architecture behind this translator is what we call phase-transition-aware valuation modeling. It recognizes that biotech enterprises move through discrete developmental stages at which the composition of value, the identity of the relevant market participants, and the economic function of common stock all change discontinuously. The model weights between current value methods and option-based allocations as a function of stage, calibrated to empirical clinical success probabilities and the progressive transfer of value from human capital to intellectual property. It extends the standard discount for lack of marketability to capture effort contingency and information asymmetry, the dynamics that made this story’s strike price dispute irresolvable. And it provides the principled calibration guidance that current regulatory frameworks acknowledge is needed but leave entirely to practitioner judgment.

This is the framework RNA Advisors has built, specifically for life sciences companies navigating the complexities of equity compensation, financing, and governance across the developmental lifecycle. It integrates nested utility analysis, which maps the structurally different objectives of each participant at the table, with value composition transfer modeling, which tracks how enterprise value migrates from people to intellectual property through clinical milestones. The result is a methodology that serves every stakeholder: the investors who need audit-defensible rigor, the executives who need compensation structures that actually recruit and retain, and the employees whose silent equity stakes depend on getting this right.

The science in this story is still good. The scientists who stayed are still at work. The patients who need the therapy are still waiting.

The framework that failed them doesn’t have to be the only one available.

About RNA Advisors

RNA Advisors helps biotechnology and pharmaceutical companies translate scientific and clinical value into investor-ready narratives. Our valuation frameworks are built specifically for milestone-driven biotech—modeling phase transitions/value inflection points explicitly, aligning methodology to the actual market participants at each stage of development, and preserving the optionality that standard approaches tend to flatten. Through rigorous financial modeling, market research, and analytical frameworks built for the unique dynamics of life science assets, we bridge the gap between breakthrough science and effective capital formation.